May 5, 2020

Layoffs Fray Health Insurance Network

The majority of Americans who have health insurance – some 150 million workers – get their coverage through their employers. But this network has suddenly developed a big hole in the midst of a pandemic.

The economic shutdown that is suppressing the coronavirus has thrown nearly 30 million people out of work – and taken away their health insurance. Millions more are expected to be laid off.

About 10 percent of the U.S. population did not have health insurance in 2018, Kaiser’s most recent estimate. This share will certainly increase sharply, but how high it goes and how quickly the situation will improve is hard to predict, given all the uncertainties, said Jennifer Tolbert, director of state health reform for the Kaiser Family Foundation.

The Affordable Care Act (ACA) does provide options that were unavailable to people who lost their jobs during the 2008-2009 recession. Even so, “there are still so many ways that people can lose insurance,” Tolbert said.

The coronavirus “highlights the still-existing gaps in our healthcare system and coverage,” she said.

Under the ACA, the newly unemployed potentially have two options: purchasing private policies on the state insurance exchanges or enrolling in the Medicaid program for poor and very low-income people.

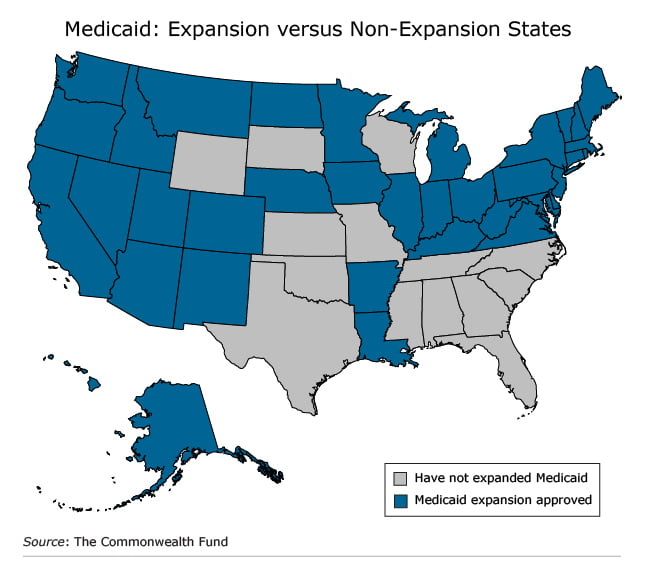

Medicaid enrollment is available year-round for the newly unemployed and for low-paid workers whose hours have been cut, causing them to lose the insurance they had when they were full-time. But this program is not an option for thousands of laid-off workers in 14 states, including Florida and Texas. They will slip through the cracks, because their states have declined the ACA option to extend their programs to cover more residents.

Medicaid enrollment is available year-round for the newly unemployed and for low-paid workers whose hours have been cut, causing them to lose the insurance they had when they were full-time. But this program is not an option for thousands of laid-off workers in 14 states, including Florida and Texas. They will slip through the cracks, because their states have declined the ACA option to extend their programs to cover more residents.

Medicaid historically has provided health insurance for low-income parents with dependent children. Under the ACA, most states did expand their programs and now include adults who do not have children. The ACA also expanded coverage by increasing the income ceiling for Medicaid eligibility to 138 percent of the federal poverty level.

If unemployment benefits disqualify someone for Medicaid, they may buy coverage on the state insurance exchanges. Under a provision of the ACA passed in 2010, they do not have to wait until healthcare.gov’s open enrollment period in November to buy a policy on the exchanges if they lost their employer health insurance when they were laid off.

Due to the heightened anxiety during the coronavirus, 11 states and Washington D.C. took an extra step and opened their insurance marketplaces to all uninsured individuals immediately. The 11 states are California, Colorado, Connecticut, Maryland, Massachusetts, Minnesota, Nevada, New York, Rhode Island, Vermont, and Washington.

There are also non-ACA options for health insurance. Laid-off workers can be added to a spouse’s employer policy. Others may want to continue their former employer’s coverage under the federal COBRA law that applies to employers with at least 20 workers. But COBRA policies are expensive, because they are not subsidized by employers, and many cash-strapped former employees will decide they can’t afford to pay the entire premium.

Kaiser said many people who relied on employer coverage will remain uninsured, because they “won’t know where to go or how to apply” for the government insurance options.

Despite significant improvements in coverage over the past decade, the nation’s health insurance network is still not up to the task of covering everyone, even in a pandemic.

Read more blog posts in our ongoing coverage of COVID-19.

Squared Away writer Kim Blanton invites you to follow us on Twitter @SquaredAwayBC. To stay current on our blog, please join our free email list. You’ll receive just one email each week – with links to the two new posts for that week – when you sign up here. This blog is supported by the Center for Retirement Research at Boston College.

I’m a professional writer with over 10 years of experience in the crypto industry. I have written for numerous publications, includingCoinDesk, Crypto Briefing, and The Block. My work has been featured in Forbes, Business Insider, and Huffington Post. I’m also a thought leader in the space and my insights into the industry are highly appreciated by readers worldwide.

Comments are closed.