In a previous post, I recommended it would be wise to get a life insurance policy before you see a doctor for any non-life threatening health issue. By locking in a life insurance policy first, you reduce your chances of life insurance companies raising your premiums due to additional health issues on your medical record.

In 2017, I went to see an overzealous sleep doctor who diagnosed me with snoring, a deviated septum, and sleep apnea. To pad his bill, he also recommended I try a CPAP machine and go through a series of sleep tests. I figured why not since my health insurance would pay for everything. I hadn’t seen a single doctor in years, despite paying over $20,000 a year in premiums.

After I did all the sleep tests, I went to check with my existing life insurance company on renewing my $1 million, 10-year term policy I took out in 2013. A term life insurance policy is appropriate for most people who want life insurance. Unfortunately, I discovered the renewal premium would jump from $40/month to $450/month!

Part of the increase in premium was because I was four years older and over 40. There seems to be a life insurance premium jump at 40 and 45. But most of the reason for the jump was due to the sleep apnea mark on my medical record.

After the disappointing news, I thought my life insurance options were over once my term policy expires in 2023. Therefore, since hearing about the higher renewal premiums, I made it my mission to boost my wealth by at least $1 million before the $1 million term policy runs out.

As it turns out, I do have a way to continue getting life insurance based on my old “excellent athletic” rating I received in 2013 when I first got my term policy. The official term for the top life insurance rating is called “Preferred Plus” followed by Preferred, Standard Plus, and Standard.

This post is pertinent for those who:

- Want to continue having life insurance coverage, but are facing a much higher term life insurance rate upon renewal

- Want to understand the various nuances of a permanent life insurance policy

- Want to understand who permanent life insurance is for

- Want to see examples of how much a universal life insurance policy costs

- Have always held a negative assumption about permanent life insurance, but can’t elaborate why beyond higher premiums

Convert Term Life Into Permanent Life To Keep Your Rate Class

The one thing I’ve done extensively during shelter-in-place is learn as much as possible about the various life insurance options out there to protect my family. One interesting fact is that some term life insurance policies can be converted to permanent life insurance policies.

Therefore, I immediately called my life insurance carrier to see if this was true for my policy. Fortunately, they said yes. Not only could I convert my term life insurance policy into a permanent life insurance policy, but the new premium would also be based on my Preferred Plus rating from 2013. Further, I would not have to do another medical exam!

Having a medical exam where someone comes to your house to collect your blood and urine is probably the most frequent reason cited as to why people either don’t have any life insurance or only have a modest life insurance amount to avoid the medical exam.

If you are getting a $1 million or greater life insurance policy, chances are high that you will need to get your blood drawn and your urine collected. Here are some other no medical exam life insurance solutions.

As the father of a three-year-old and a five-month-old, I’m excited to be able to have the OPTION to have continued life insurance coverage based on my Preferred Plus rate at least until they graduate from college or become financially independent adults.

Let’s look at the benefits of permanent life insurance, also commonly referred to as whole life insurance or cash value life insurance. Yes, all the terms can get confusing.

Benefits Of Permanent Life Insurance

1) Lifetime Protection

Instead of having a term policy that has an expiration date, permanent life insurance covers your entire life so long as premiums are paid. Having a permanent life insurance policy helps provide peace of mind through all stages of life, whether you are just starting out, raising a family, or living in retirement.

In 2013, I got a 10-year, $1 million term life insurance policy because while I no longer had a job, I still had a ~$1 million mortgage. If I died, I didn’t want my wife to be saddled with so much debt.

At the time, we were also uncertain about whether or not to have kids. Had I known we would have a kid in 2017 and another in 2019, I would have gotten at least a 20-year policy.

With a permanent life insurance policy, you won’t have to worry about all the different curve balls life may throw your way.

2) Flexibility

Basically, there are four different types of permanent life insurance to address different goals:

The main difference in all these types of permanent life insurance policies is how the cash value portion is invested. The cash value is the portion of a permanent life insurance policy that gets built up over time based on the premiums you pay.

In my case, I’m able to convert my term life insurance policy into a universal life policy, a conservative type of permanent life insurance. Universal life provides the ability to adjust payment amounts and death benefits to satisfy changing goals, needs, and budgets.

When you have enough cash value built up, you can even stop paying premiums by using your cash value to keep the policy active.

3) Cash Accumulation

Permanent life insurance provides a cash account that can supplement education and retirement needs while benefiting from tax-deferred growth (similar to a 401(k)) at competitive interest rates.

The cash value is the main difference that differentiates a term life insurance policy from a permanent life insurance policy. The premiums you pay for a permanent life insurance policy go towards paying for the death benefit amount and the cash value.

Given the tax-advantageous growth of the cash value, getting a permanent life insurance policy is another way for people to build wealth and manage their estates.

Why Doesn’t Everybody Get A Permanent Life Insurance Policy?

One of the main reasons why people don’t consider a permanent life insurance policy is because it’s more difficult to understand compared to a term life insurance policy.

You can think about a term life insurance policy similar to paying rent for an apartment. Your rent pays for shelter each month and nothing more. Once the lease is over, you can either extend your lease or move out if you no longer desire to pay the rent. You do not build equity with rent.

A permanent life insurance policy is kind of like paying an amortizing mortgage. Part of your mortgage payment goes to paying down principal and building equity (cash value) and the remaining portion goes to paying interest (the death benefit). Over time, your cash value (equity) grows as it is reinvested.

The second reason why permanent life insurance isn’t very popular is due to not knowing all the options. I’ve always known about permanent life insurance, but I stopped thinking about it after I got my term life insurance policy. Most people don’t care to research their life insurance options until it’s needed, e.g. bought a home with a mortgage, had kids, came into a lot of wealth, got a bad disease.

The final reason, and probably the main reason is the cost. Just like how it’s usually cheaper to pay rent or an interest-only mortgage, it’s cheaper to just pay for term life insurance rather than permanent life insurance.

When you have to also pay to build up your cash value, permanent life insurance premiums are much higher.

Example Of A Universal Life Insurance Policy

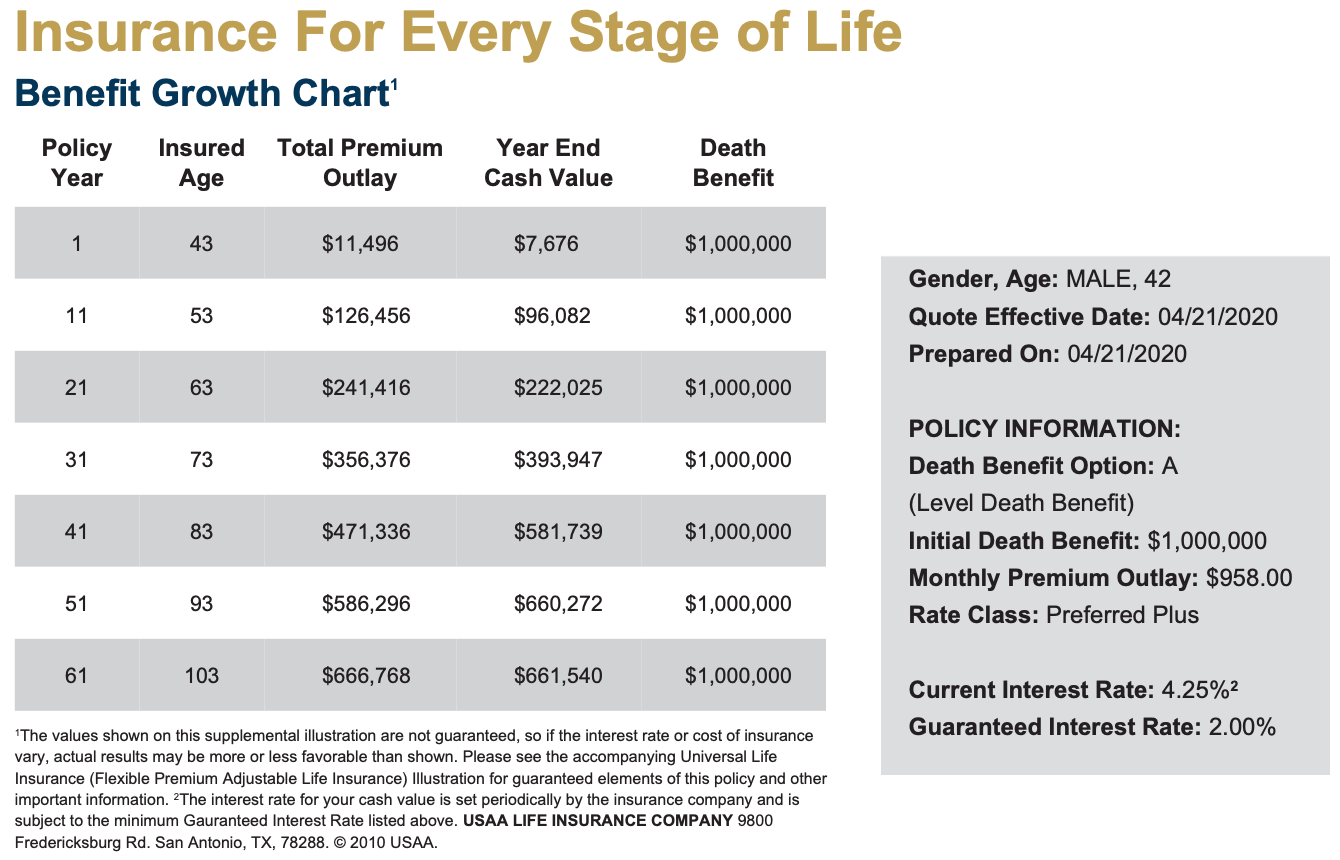

Below is an example of an “option A” universal life insurance policy I received after talking with the insurance agent for an hour. This policy is what I’ll get if I convert 100% of my $1 million term life insurance policy into a universal life insurance policy and keep my same Preferred Plus rating.

To reduce my premium, I can convert a smaller portion of the $1 million term policy into a permanent life insurance policy and keep the remaining death benefit amount until my term life insurance policy runs out in 2023.

For example, I could convert $250,000 of my $1 million term life insurance policy into a universal life insurance policy and keep the remaining $750,000 until it expires in 2023. However, the longer I wait, the higher the premium and the less time I get to build the cash value given rates go up with age.

Let’s study this universal life insurance benefit growth chart from USAA carefully.

As you can see from the chart, my universal life insurance policy will cost $958/month! That’s obviously much higher than my existing $40/month, so why the heck would I go this route?

The main reasons are as mentioned above: 1) building up the cash value, 2) having a permanent life insurance policy, and 3) being able to get the best premium rate based on my Preferred Plus 2013 health exam and not my suboptimal 2017 health examination.

Although my monthly premium is $958/month, $640/month of that amount is used towards building my cash value. Therefore, you can say my monthly life insurance premium to cover the death benefit is only $318/month compared to the $450/month I was quoted in 2017 when I tried to renew.

I’m guessing if I check with my existing life insurance provider again with a medical exam, my new $1 million term life insurance renewal premium might be over $550/month. Therefore, converting to a universal life insurance policy might actually save me over $200/month in death benefit coverage.

But to say that my life insurance premium is only $318/month is understating the value of this permanent life insurance policy due to the potential of tax-deferred growth in the cash value, the guaranteed minimum rate of return, plus the fixed monthly premium cost for the rest of my life.

This universal life insurance plan has a guaranteed minimum 2% annual rate of return on the cash value. 2% compares favorably with the 10-year bond yield at under 0.8% and the Fed Funds rate at 0% – 0.125%. The best online bank interest rate you can get currently is around 1.25%. Remember, everything is relative when it comes to finance.

Further, there is the potential for the cash value to return greater than a 2% annual return. The current rate of return for the cash value is 4.25%, which at one point, compared very favorably when the S&P 500 was down 32% in March 2020.

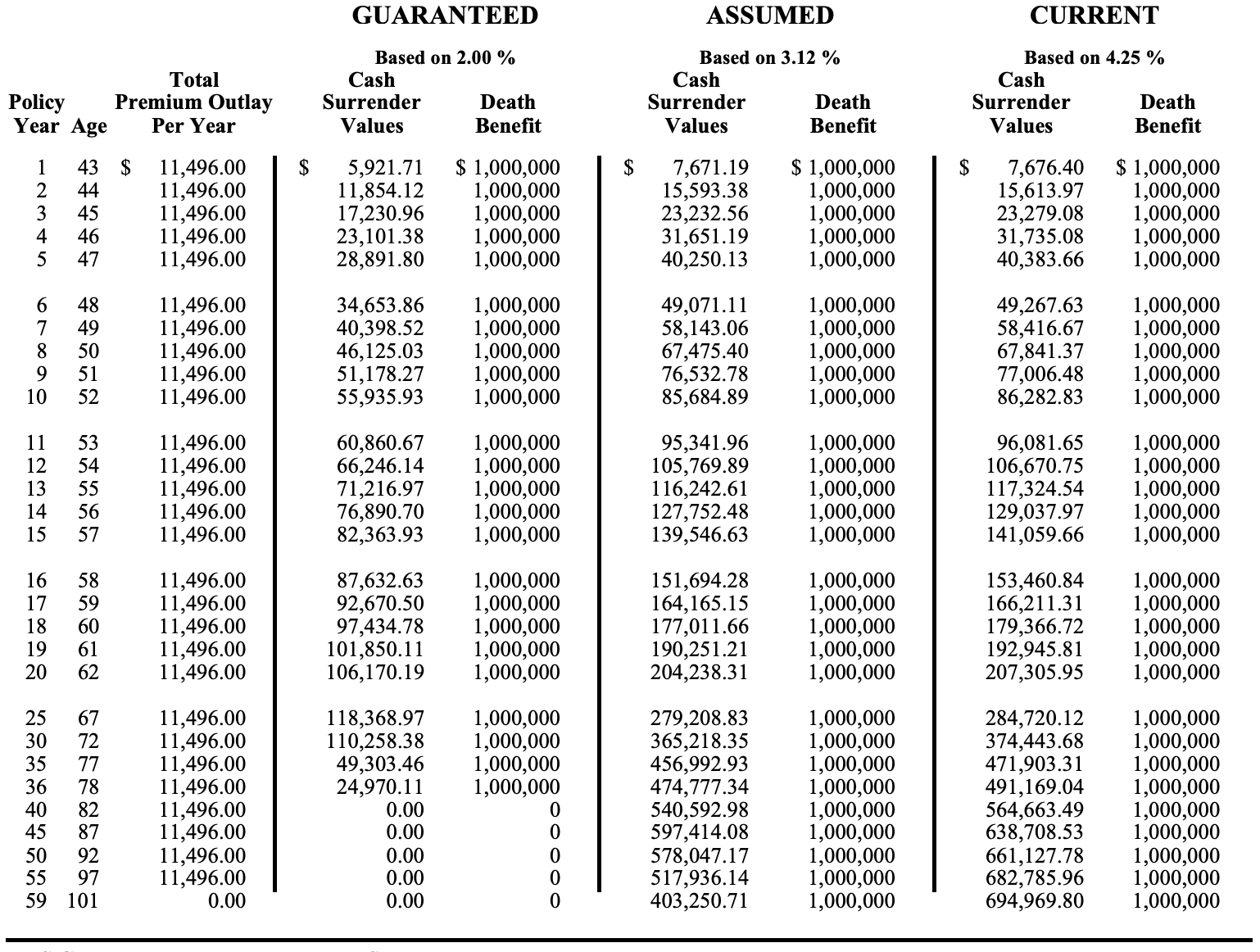

In the below chart, take a look at the growth of the cash value based on a 2%, 3.12%, and 4.25% annual rate of return.

As you can see from the chart above, over time, the cash value really starts to compound. The cash value can be used to boost the death benefit, generate an income stream, pay for the universal life insurance premium, or be taken out as a loan.

However, there is one big issue with “Option A” universal life insurance. If you die, your beneficiaries only get the death benefit amount of $1 million and none of the remaining cash value! The remaining cash value is kept by your life insurer.

To avoid having the life insurance company keep all your accumulated cash value, you should call up your life insurance company and see if you can exchange the cash value for a higher death benefit. Ask them what other options you have for using the cash value before death.

The other option for those who want their beneficiaries to keep the cash value is to choose “Option B” universal life insurance.

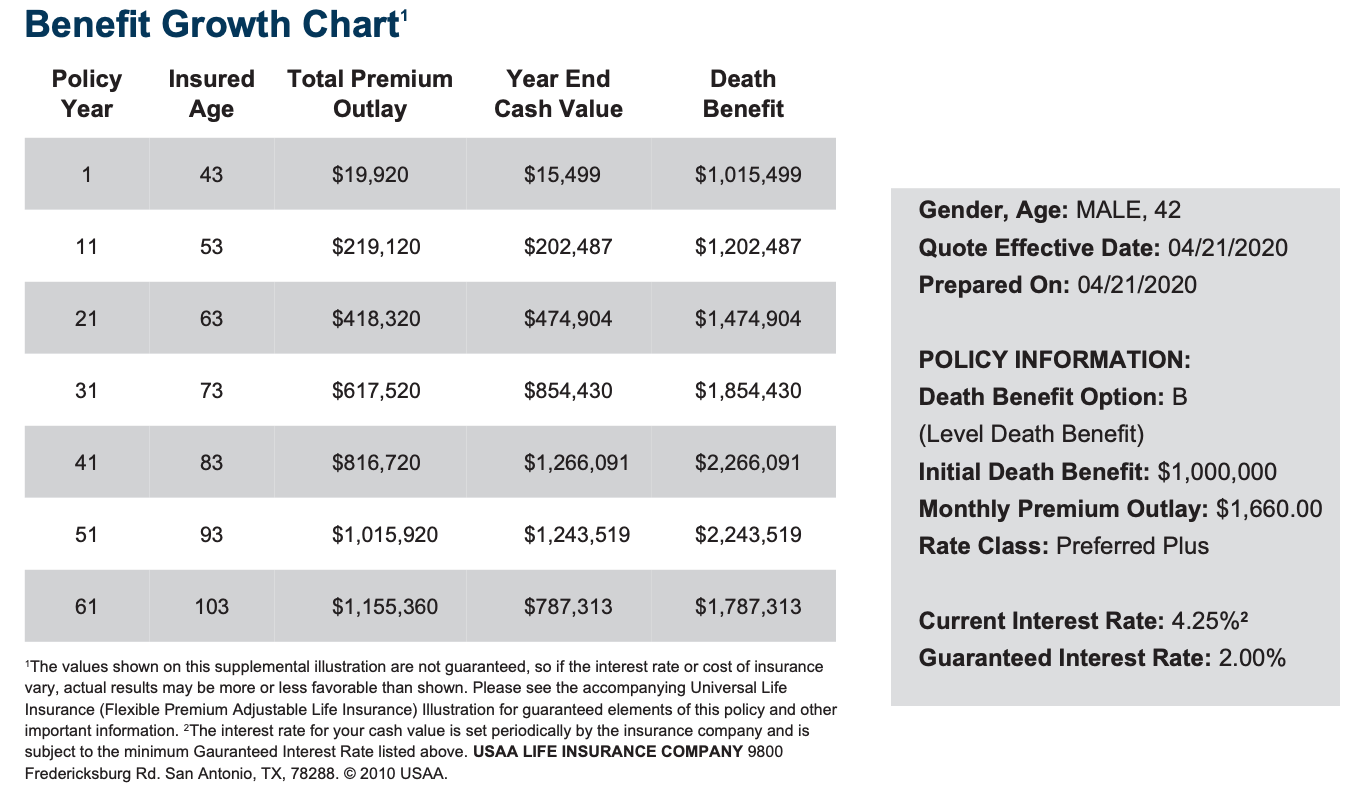

Option B Universal Life Insurance

With “Option B” universal life insurance, your beneficiaries will receive your death benefit and accumulated cash value. Of course, there is no free lunch. Option B premiums are even higher. Let’s look at the information below.

With Option B, my monthly premium goes up to an impressive $1,660. $1,291 of the $1,660 goes towards building cash value. Therefore, the cost of the $1 million death benefit is $369/month on average for the first year. Despite the much higher premium, I never have to worry about losing all the cash value. Instead, all the cash value will go to my beneficiaries.

Below is a table that shows the growth of the cash value using a 2% return, 3.12% return, and a 4.25% return. The death benefit columns are now the summation of the $1 million death benefit plus accumulated cash value. After 40 years, the cash value grows to over $1 million, meaning if I die at 82, I will leave over $2 million to my beneficiaries, tax-free.

Who Should Get Permanent Life Insurance?

Hopefully, my two universal life insurance policy examples illustrate an option if your term life insurance premium is going way up due to a health issue or older age. By converting to a permanent life insurance policy, you get to keep the higher rating that you once received years ago.

Let’s be frank, a permanent life insurance policy costs a lot more than a term life insurance policy. As a result, most people will just get a term, which is the most efficient and cost-effective way to go. There are just incidences, where life changes, health changes, and needs changes beyond the term limit.

My favorite way to get an affordable term life insurance policy is with PolicyGenius, a life insurance marketplace that matches the best life insurance offers based on your application.

Here are the types of people who should consider getting a permanent life insurance policy:

- Parents with lifelong dependents, e.g. a child with down syndrome or severe cerebral palsy (bless them all).

- Parents who have gone through a difficult life and want lifelong peace of mind for themselves and for their beneficiaries.

- Parents or debtors who work in hazardous industries with unknown future health risks.

- People who plan to have a much higher net worth and want to conduct estate planning to minimize taxes upon death.

- People who contribute the maximum to their 401(k) and other tax-advantageous retirement accounts and want another way to grow wealth in a tax-advantageous manner.

If at least a couple of these conditions pertain to you, getting a permanent life insurance plan or converting your term life insurance plan to a permanent life insurance plan may make sense. Otherwise, going with the plain vanilla term life insurance plan is your best bet.

My Life Insurance Plan

As for me, I like having a new way of conservatively growing my wealth in another tax-advantageous manner. After all, I’ve maxed out my 401(k) and now Solo 401(k) since 2000, contribute to two 529 plans, and neither my wife nor I have stable day job income.

Because we currently have excess cash flow due to passive retirement income and online income, contributing money to a permanent life insurance policy solves two goals of insuring for life and investing more for our future.

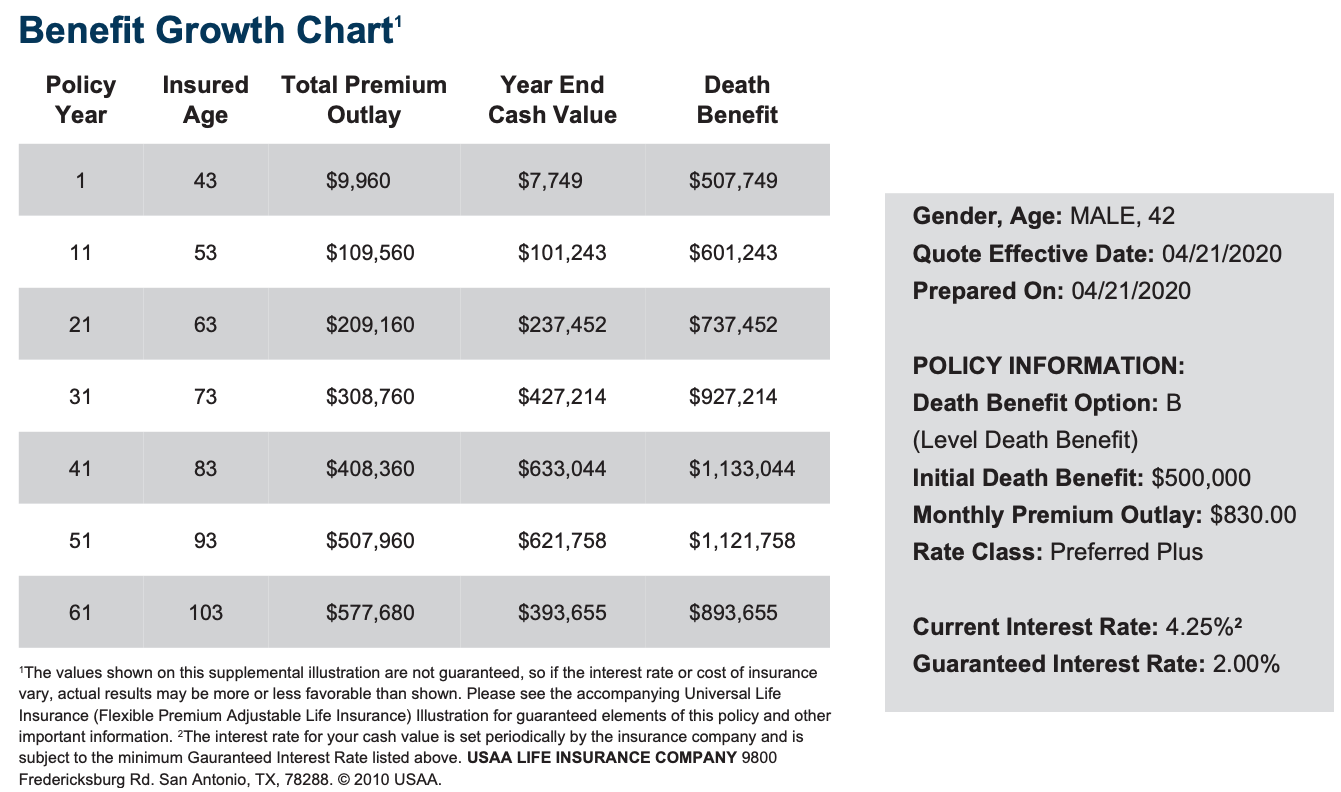

Because I place a premium on peace of mind, I’m strongly considering converting at least a portion of my $1 million term life insurance policy into a permanent life policy before it runs out in 2023. It feels good being able to lock in my Preferred Plus rating from 2013 since I inaccurately forecasted my future.

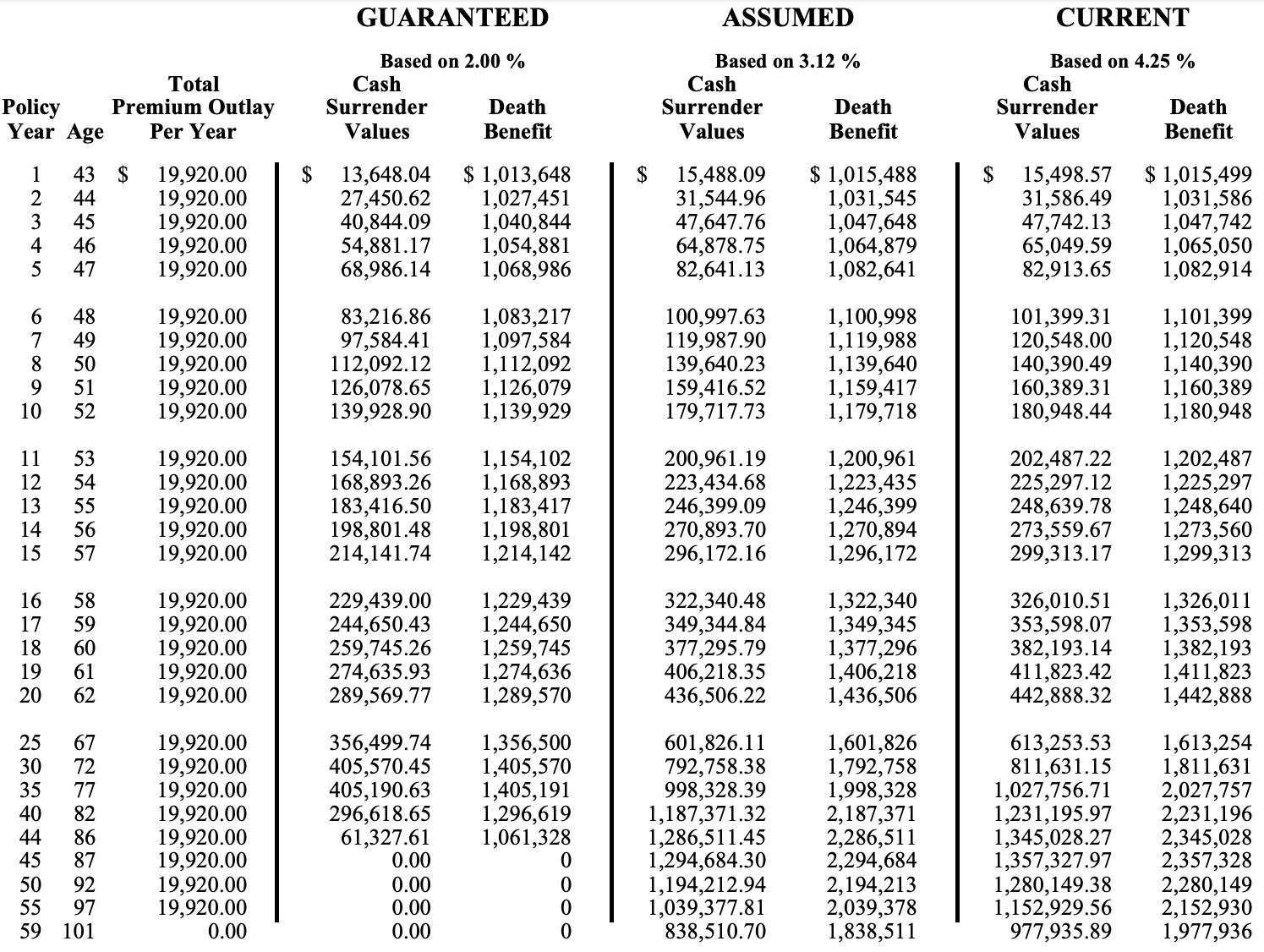

Below is the benefit growth chart example if I convert $500,000 of my $1 million term policy into an option B universal life policy, where my beneficiaries get the death benefit and the cash value.

My monthly premium outlay drops to a more affordable $830/month from $1,660/month and the death benefit reaches over $1 million after 41 years assuming relatively conservative returns. If the goal is to provide an overall death benefit of $1 million, then this is one way to go.

Although a life insurance policy is an act of kindness for my family, a life insurance policy also provides me peace of mind if something bad were to happen.

Finally, before you get a permanent life insurance policy, you should estimate the value of your estate currently and at various times in the future. If your estate will significantly blow past the estimated estate tax exemption amount, then trying to build more wealth through a permanent life insurance policy isn’t as effective.

That said, if you have enough cash flow to easily afford a permanent life insurance policy, then there’s not much downside in building more wealth in this tax-efficient manner.

For most folks, getting a term life insurance policy is good enough. You can apply with well-known providers one-by-one, or you can go through PolicyGenius and have qualified providers vie for your business.

I’m having my wife go through the process with PolicyGenius right now to up her life insurance amount. She’ll report back with her experience and findings.

Readers, anybody have a permanent life insurance policy? If so, what do you think of it and what would you have done differently? Do you think getting a permanent life insurance policy is a good idea? How can you use an irrevocable trust to shield the permanent life policy from estate taxes?

Before you completely disregard the value of a permanent life insurance plan, please provide a solution for someone who wants or needs life insurance beyond his or her term policy limit, but is facing a 10X increase in policy premiums due to health issues. This is a solutions-focused website that tries to get people to see the other side.

I’m an experienced writer and commentator on all things cryptocurrency. I have been involved in the crypto community since early 2017 and have been writing about Bitcoin, Ethereum, and other digital assets since then. In addition to being a journalist, I have written two books on cryptocurrency investing: “Cryptoassets: The Innovative Investor’s Guide to Bitcoin and Beyond” (2017) and “The Art of Cryptoasset Investing” (2018). I’m a regular contributor to Forbes’ Cryptocurrency & Blockchain section, where I write news and analysis on the latest developments in the space.

Comments are closed.